How BNPL Affects Your Credit Score in 2026 (What's Actually Changed)

By Jason Wilcox

The relationship between Buy Now Pay Later and your credit score has changed more in the past year than in the entire history of BNPL. New scoring models, new reporting standards, and new regulations are rewriting the rules.

If you've been confused about whether your Afterpay or Klarna payments actually show up on your credit report, you're not alone. The answer used to be simple: they don't. Now it's complicated — and getting more complicated by the month.

Here's what's actually happening in 2026, provider by provider, with no speculation or guesswork.

Which Providers Report to Credit Bureaus (And Which Don't)

This is the question everyone asks first, so let's get straight to it. As of early 2026, here's where each major BNPL provider stands:

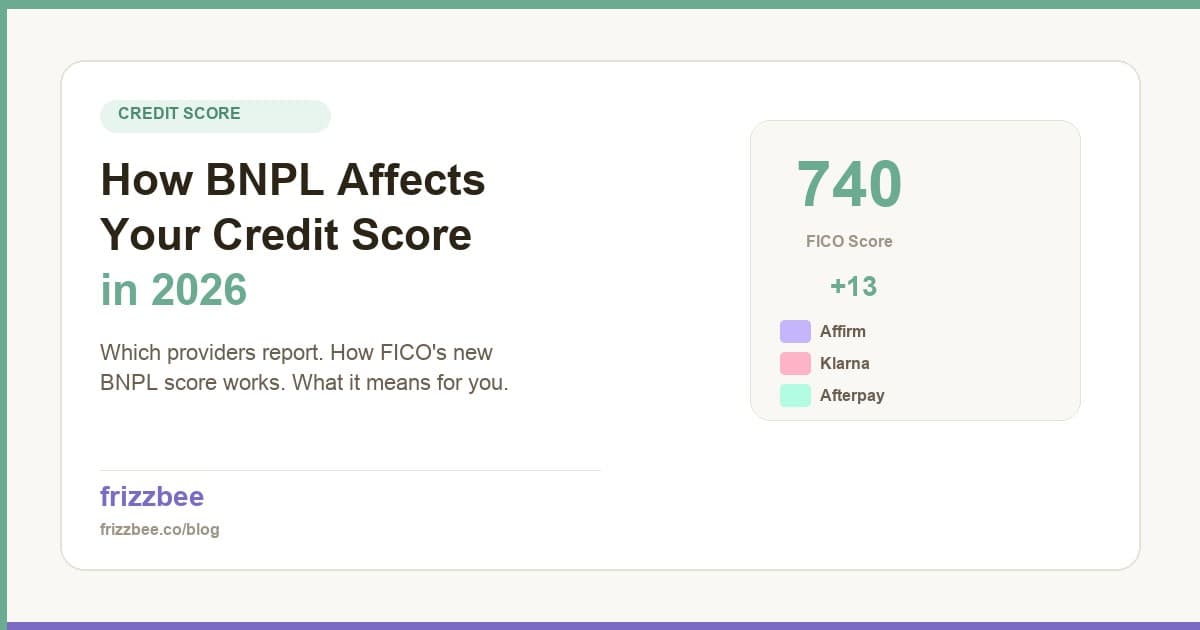

Affirm reports ALL products — including Pay in 4 — to Experian and TransUnion. Both on-time and missed payments are reported. If you use Affirm, every payment you make (or miss) is building your credit history. Affirm is the most transparent BNPL provider when it comes to credit reporting.

Klarna reports longer-term financing to TransUnion and Experian, but does not report to Equifax. Klarna has been cautious about reporting short-term BNPL data like Pay in 4, saying they won't do so until credit scoring models can handle it properly without hurting consumers.

Afterpay does NOT report to US credit bureaus. They've explicitly stated they won't report "until we see concrete evidence that BNPL data reflecting responsible payment behavior will help, not hurt, the credit scores of our customers." But there's a massive caveat: accounts sent to collections WILL be reported. More on that below.

Sezzle offers optional opt-in reporting. If you want to build credit with Sezzle, you can choose to have your payments reported. By default, only delinquent or collections accounts are reported.

Zip does not report to credit bureaus for standard use. Collections are reported.

PayPal Pay Later reporting varies by product. Their longer-term financing products may be reported, but standard Pay in 4 generally is not.

The Big Change: FICO Score 10 BNPL

This is the headline development of 2026.

In June 2025, FICO announced the launch of FICO Score 10 BNPL and FICO Score 10 T BNPL — the first credit scores from a leading scoring provider to incorporate BNPL data. This is a big deal because FICO scores are used in the vast majority of US lending decisions.

FICO built these models from a year-long study with Affirm on more than 500,000 consumers. The key design decision: instead of treating each BNPL loan as a separate new credit line (which would tank your score by making it look like you opened 15 new accounts), the model aggregates multiple BNPL loans together.

The early testing results were encouraging. Most users with 5 or more Affirm loans saw their scores either increase or stay stable under the new model. Typical score movement was approximately plus or minus 10 points. People who paid on time generally saw a boost; people who missed payments saw a small dip.

As of early 2026, FICO says these models "will be made available at the credit bureaus concurrently with BNPL data being made available by the credit bureaus at scale." Translation: it's coming, but it depends on the bureaus getting their BNPL data infrastructure in place first. These new scores will be offered alongside existing FICO scores at no extra cost to lenders.

How the Credit Bureaus Are Handling BNPL Data

Each bureau is taking a different approach, which adds to the confusion:

Experian launched a separate "Buy Now Pay Later Bureau" that stores BNPL data separately from your core credit data. The idea is to protect your existing score while building out BNPL-specific reporting. They're planning real-time reporting for BNPL transactions.

TransUnion keeps BNPL data separate within credit files for now. They're planning bi-weekly reporting (compared to monthly for traditional credit accounts) and have said full integration will "take several years."

Equifax is the most aggressive. They already allow BNPL providers to report pay-in-4 loans, and unlike the other two, Equifax CAN include BNPL data in core credit score calculations right now. Their research found that consumers who paid BNPL on time saw an average FICO increase of 13 points.

How BNPL Can Hurt Your Credit

Let's be clear about the risks. Even with the new scoring models designed to be fair, BNPL can still damage your credit in several ways:

Missed payments from providers that report. If you use Affirm and miss a payment, that's a negative mark on your Experian and TransUnion reports. Same goes for Klarna on TransUnion and Experian.

Collections — the big one. Here's what most people don't realize: even providers that don't report your regular payments (like Afterpay, Zip, and most others) WILL hurt your credit if your account goes to collections. And a collections account stays on your credit report for 7 years.

Hard credit inquiries. Most pay-in-4 plans use soft checks that don't affect your score. But longer-term monthly payment plans from Affirm or Klarna may involve a hard credit inquiry, which can temporarily lower your score by a few points. Multiple hard inquiries in a short period get flagged as a risk signal.

The scale of the problem is real. According to LendingTree's 2025 research, 41% of BNPL users paid late at least once in the past year, up from 34% the year before. The CFPB reported that 53.6 million consumers used BNPL in 2023, with transaction volume estimated at $70 billion in 2025 by the Federal Reserve Bank of Richmond.

How BNPL Can Help Your Credit

It's not all downside. Used responsibly, BNPL can actually build your credit:

Affirm's on-time reporting builds positive tradelines. Every payment you make on time with Affirm adds a positive data point to your Experian and TransUnion files. Over time, this builds a track record of responsible borrowing.

FICO's new model rewards responsible use. The whole point of FICO Score 10 BNPL is to recognize consumers who use BNPL responsibly. If you're paying on time across multiple plans, the new model is designed to see that as a positive signal.

The Equifax data is promising. Their study found on-time BNPL payers saw an average 13-point FICO increase. That's meaningful — enough to move you from one credit tier to the next.

Thin-file consumers benefit most. If you have limited credit history (maybe you're young, new to the US, or have avoided credit cards), BNPL reporting through Affirm or Sezzle's opt-in program can help you establish a credit file without taking on traditional debt.

The Collections Trap

This is the part most people don't understand, and it's the most important thing in this entire article.

Even if your BNPL provider doesn't report to credit bureaus, they can still destroy your credit. Here's how: you miss enough payments, the provider freezes your account, and eventually they sell your debt to a collection agency. That collection agency reports to the credit bureaus.

So the fact that Afterpay "doesn't report to credit bureaus" gives some people a false sense of security. Yes, your on-time payments won't help your score. But your worst-case scenario — collections — will absolutely wreck it. A collections account can drop your credit score by 100 points or more, and it stays on your report for 7 years.

This is why tracking your payments matters even when your provider doesn't report. Missing a $50 Afterpay payment might seem low-stakes in the moment, but if it spirals into collections, the credit damage far outweighs the original purchase.

What You Should Do Right Now

Here are the practical steps, regardless of which providers you use:

1. Know which of your providers report. If you use Affirm, treat every payment like a credit card payment — it directly affects your score. If you use Afterpay, the stakes are lower for individual payments but the collections risk is still real.

2. Set up payment reminders or autopay. The single most important thing you can do is pay on time. Set alerts 3 days before each due date. Better yet, make sure the funds are in your account before the payment is due.

3. Track all your plans in one place. When you're juggling Afterpay, Klarna, and Affirm across different apps, it's easy to lose track. A tool like Frizzbee puts every payment from every provider on one dashboard with reminders before each due date. Visibility prevents surprises.

4. Consider opt-in reporting. If you're trying to build credit and use Sezzle, opt into their credit reporting. If you use Affirm, you're already being reported — make that work for you by never missing a payment.

5. Don't over-extend. The CFPB has flagged that many BNPL users carry more debt than they realize because each plan feels small on its own. Keep your total BNPL payments under 15% of your monthly income. Check out our guide on how many BNPL plans is too many for benchmarks.

6. Check your credit reports. If you use Affirm or Klarna, check your credit reports (free at annualcreditreport.com) to verify your payments are being reported correctly. Errors happen, and disputing them early is important.

The Bottom Line

BNPL and credit scores are in a transition period. The old answer — "BNPL doesn't affect your credit" — is no longer true for many providers and will become less true as FICO 10 BNPL rolls out.

The new reality: Affirm reports everything. Klarna reports most things. Everyone else reports collections. And FICO is building scoring models that will eventually incorporate all of it.

If you're using BNPL responsibly — paying on time, not overextending, keeping track of your plans — these changes will likely help you. If you're missing payments and hoping nobody notices, the window for that is closing fast.

The smartest move is to treat every BNPL payment like it matters to your credit, because increasingly, it does. For a deeper dive into how each provider handles credit, check out our BNPL Credit Score Impact guide.